Occupancy is stable. Census is healthy. Sales teams are meeting targets. From the outside, everything appears to be working.

Then someone asks a simple question:

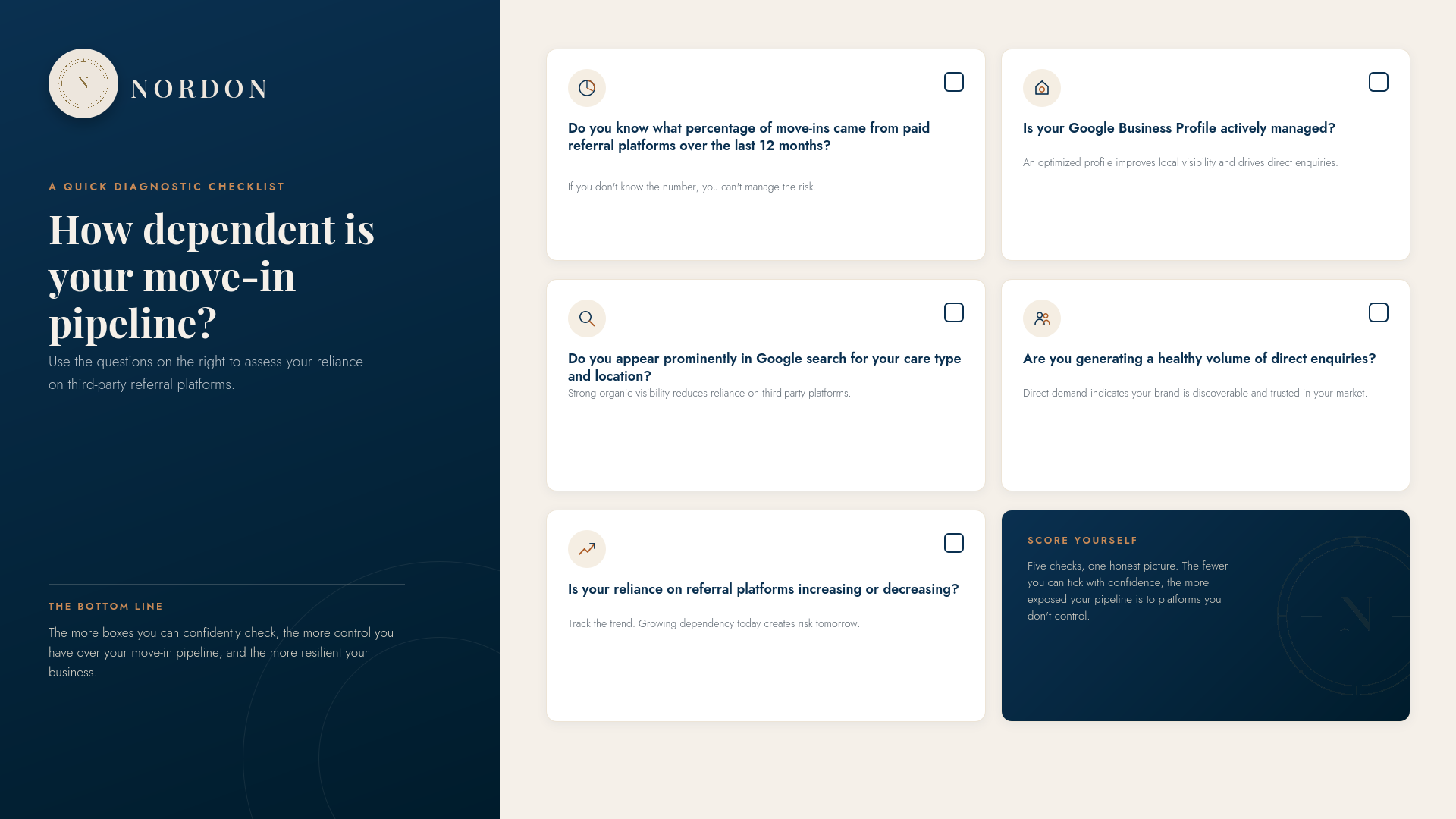

Where did your move-ins actually come from over the last 12 months?

The answer often tells a very different story.

If most new residents originated from a single referral platform, the community is not generating its own demand. It is renting demand from a third party that earns a fee every time it delivers another resident.

That distinction matters because a full building does not necessarily indicate a resilient marketing engine. It may simply indicate that someone else owns the pipeline.

Key Takeaways

- A full community doesn't always mean a resilient move-in pipeline.

- Heavy reliance on referral platforms creates risks that often go unnoticed.

- Understanding your channel mix is the first step towards reducing dependency.

- The question isn't whether your community is full. It's who owns the demand.

What is Aggregator Dependency?

Aggregator dependency is the degree to which a senior living community relies on third-party referral platforms such as A Place for Mom, Caring.com, and Seniorly to generate move-ins instead of attracting families through its own marketing channels.

These companies provide a legitimate and valuable service. They help families navigate one of the most important decisions they will ever make and connect them with suitable communities.

The issue is not whether operators should use them. The issue is what happens when they become the dominant source of new residents.

Most referral platforms charge operators a fee of approximately 8% to 12% of first-year resident revenue.

For an assisted living or memory care resident generating $60,000 in annual revenue, a 10% referral fee equates to approximately $6,000 per move-in.

At 30 referral-generated move-ins per year, that represents roughly $180,000 in referral fees. At 40 move-ins, the cost approaches $240,000.

Those fees come directly out of operating revenue. They also repeat indefinitely because every resident who moves out eventually needs replacing.

Why is Aggregator Dependency a Business Risk?

The referral fee is the visible cost. The larger issue is structural.

When families discover a community through an aggregator, the relationship often begins with the platform rather than the operator. The community becomes one option within someone else's ecosystem instead of establishing a direct connection from the beginning.

Heavy reliance on referral platforms can also conceal weaknesses in a community's own marketing. Organic search visibility is often limited, Google Business Profile receives little attention and paid search may be inactive. Families searching for care in the local market find aggregator websites before they ever reach the operator's own website.

Strong occupancy can disguise those shortcomings for years.

The pipeline is also vulnerable in ways that financial reporting rarely reveals until after performance starts to decline. Referral fees can increase. Platform algorithms can change. Competing communities may receive greater visibility. None of those decisions sit within the operator's control, yet each has the potential to affect future occupancy.

Perhaps the biggest difference is that referral fees never create a lasting asset.

Investment in owned marketing channels can strengthen search visibility, improve local rankings and increase direct enquiries over time. Referral fees simply purchase the next resident. Once that resident leaves, the process begins again.

What Does a Healthy Channel Mix Look Like?

Using referral platforms is not the problem. Relying on them is.

For a well-marketed, stabilised community, paid referral platforms should generally account for around 10% to 20% of move-ins, while most enquiries should come through channels the operator owns and controls.

| Owned Demand | Rented Demand |

|---|---|

| Community owns the relationship with prospective families | The first relationship belongs to the referral platform |

| Marketing investment strengthens future lead generation | Referral fees repeat with every new resident |

| Greater visibility through Google Search and Google Business Profile | Families often discover the community through third-party platforms |

| More control over enquiry volume | Greater reliance on another company's pricing and priorities |

Reducing dependency does not require eliminating referral platforms. Across one senior living portfolio of 38 communities, aggregator dependency fell from 80% to 58% over approximately three years through sustained investment in owned marketing infrastructure.

The objective is balance. Aggregators should remain one acquisition channel, not the entire acquisition strategy.

When Do Aggregators Make Sense?

There are situations where referral platforms provide genuine value.

Lease-up, repositioning, and occupancy recovery often require rapid enquiry volume. Referral platforms can help communities rebuild census while owned marketing channels mature.

Maintaining accurate profiles on major referral platforms also has increasing value as AI-powered search becomes more common. Platforms such as ChatGPT, Google's AI Overviews, and Perplexity frequently reference established senior living directories when generating recommendations. Communities with complete, well-maintained profiles are more likely to appear in those results.

That does not change the broader strategy. Operators should maintain accurate listings while directing most review activity toward Google, where reviews contribute to stronger local visibility and direct trust with prospective families.

How Can You Measure Your Dependency?

One report can answer the question.

Every operator should know what percentage of move-ins over the previous 12 months came from each acquisition channel, including referral platforms, organic search, Google Business Profile, paid search, healthcare referrals, and direct enquiries.

Most senior living CRM platforms can produce this information. If that report is unavailable, it becomes difficult to understand which marketing investments are generating results.

A simple self-assessment can reveal whether dependency is becoming a concern.

- What percentage of move-ins came through paid referral platforms?

- Is organic search traffic growing year over year?

- Is your Google Business Profile actively managed?

- Does your community appear prominently when families search for your care type and location?

Communities that struggle to answer those questions often discover they have become more dependent on referral platforms than they realised.

The Question Every Operator Should Ask

Most communities with a strong care offering can fill available units.

The more important question is how they fill them.

Communities that generate direct demand build a commercial asset that becomes more valuable over time. Search visibility improves, more families discover the community directly, and marketing investment continues to deliver returns long after the initial spend.

Communities that rely primarily on aggregators operate differently. Occupancy may remain healthy, but each future move-in depends on another referral and another fee. The pipeline remains tied to another company's business model and commercial priorities.

That is why aggregator dependency deserves more attention than it often receives.

It is not simply a marketing metric. It is a measure of how much control an operator has over future occupancy and future profitability.

Who Owns Your Pipeline?

Most communities can fill available units. The real question is whether they're building demand they own or renting it from someone else.

Communities with strong owned channels become more resilient over time. Their visibility improves, direct enquiries increase, and marketing investment continues to pay dividends. Communities that rely primarily on referral platforms face a different reality. Every future move-in depends on another referral and another fee.

If you don't know what percentage of your move-ins came through referral platforms over the last 12 months, that's the first number to find.

Nordon's independent diagnostics help investors, owners and operators assess channel concentration, aggregator dependency and commercial resilience before those risks appear in financial performance. Request a diagnostic to understand whether your move-in pipeline is building long-term value or simply renting demand.